How to Remove Collections Without Restarting the Reporting Clock

Trying to fix collection accounts can feel like walking through a minefield. You take action, send a letter, make a payment, or talk to a collector—then suddenly your credit report looks worse, not better. Many consumers discover too late that the way they handled a collection unintentionally triggered updates that kept the account damaging their credit longer than necessary.

This confusion isn’t your fault. Credit reporting rules are rarely explained clearly, and most advice online oversimplifies a process that is highly technical. If you’re trying to remove collections without extending their impact, understanding how the reporting clock actually works is critical.

Authority: This guide is based on over 16 years of experience reviewing, disputing, and correcting inaccurate and misleading credit reporting across all three credit bureaus.

If you want to avoid costly mistakes and get a clear plan for your own report.

start here by clicking on the following link to schedule your Free Consultation: https://api.leadconnectorhq.com/widget/groups/parker-method-group?user_id=hYwutz9Tej2kp6gpI6rH

Quick Answer

What works:

Disputing inaccurate reporting fields, monitoring bureau responses, and following up with documentation—without admitting liability or triggering new activity.

What doesn’t:

Calling collectors without a plan, making “good faith” payments blindly, or disputing without understanding which dates matter.

When professional help matters:

If a collection keeps verifying, shows different dates across bureaus, or appears to update repeatedly despite being old.

Understanding the Credit Reporting Clock

The reporting clock for collections is tied to the date of first delinquency, not the date a collection account appears on your credit report. This original delinquency date determines how long a negative account can legally remain on your report.

The problem is that many consumers believe any activity—contact, payment, or dispute—will automatically “restart” this clock. In reality, the clock does not reset easily, but reporting errors and consumer actions can create misleading updates that make the account appear newer than it should be.

That distinction matters. A collection can stay on your report for years longer than necessary if it is inaccurately updated or re-aged.

Step-by-Step: How to Remove Collections Without Extending Damage

Step 1: Pull All Three Credit Reports

Do not rely on a single monitoring app. Each bureau may display the same collection differently. You are looking for inconsistencies in:

Date opened

Date reported

Balance

Status

Ownership

Differences between bureaus are often the strongest starting point for disputes.

Step 2: Identify Which Fields Are Inaccurate or Misleading

Effective disputes focus on data, not frustration. Common issues include:

Incorrect “date opened” fields

Balances that do not match the current status

Collections reporting as “new” after being sold

Duplicate reporting by multiple agencies

These are technical errors, not arguments about fairness.

Step 3: Dispute Strategically, Not Emotionally

Disputes should challenge specific reporting fields and request verification of accuracy and completeness. Broad disputes that simply say “this is wrong” often result in quick verifications with no real review.

Step 4: Monitor Responses and Deadlines

Each bureau has its own reinvestigation process. Some respond quickly, others slowly. Missing follow-ups allows inaccurate reporting to persist.

This is where monthly monitoring and follow-up matter. One dispute cycle is rarely enough.

Step 5: Escalate When Necessary

If a collection verifies repeatedly without correcting inconsistencies, escalation may be required. Many consumers stop at the first “verified” response—even when the data is still wrong.

That’s where progress usually stalls.

Why Most People Fail at This

This section is where most DIY efforts fall apart:

They confuse payment with correction. Paying a collection does not automatically fix reporting errors.

They don’t track dates. Missed deadlines eliminate leverage.

They dispute the debt, not the data. Bureaus verify records, not personal explanations.

They stop too early. Re-verification is common and often requires follow-up challenges.

Without a structured process, consumers unintentionally keep negative accounts active longer than needed.

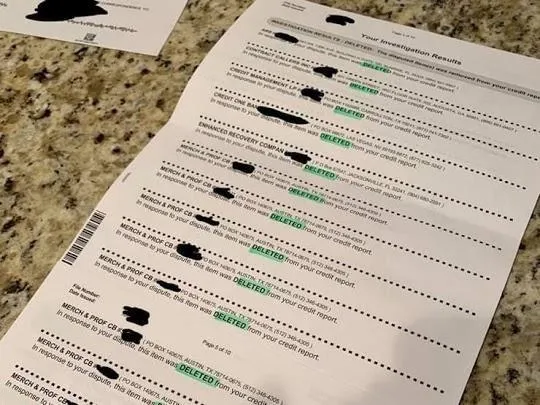

Mini Case Example (No Guarantees)

Starting situation:

A consumer had an older collection reporting differently across all three bureaus.

What was wrong:

The “date opened” field varied by bureau, making the account appear newer in some reports.

What actions were taken:

Targeted disputes challenged specific date inconsistencies and requested verification of reporting accuracy.

What improved over time:

As incorrect fields were corrected, the collection’s impact diminished as the report became more accurate. Results vary and are not guaranteed.

Frequently Asked Questions

How long does credit repair take?

Timelines vary based on the number of accounts, the accuracy of reporting, and bureau response behavior. Most progress occurs in phases, not overnight.

Do I need a monthly program?

Collections often require monitoring, follow-up disputes, and escalation. Monthly programs support consistency and accountability.

Can I cancel anytime?

Yes. Flexibility is important because every credit report is different.

Is credit repair legal?

Yes. Consumers have the right to dispute inaccurate, incomplete, or misleading credit reporting.

Will contacting a collector restart the reporting clock?

Contact alone does not reset the clock, but careless communication can lead to misleading updates if not handled properly.

Does paying a collection remove it?

Not necessarily. Paid collections can still appear unless reporting is corrected or removed.

Final CTA

Removing collections without extending their damage requires precision, timing, and follow-through. Credit repair is not a one-time action—it’s a structured process.

If you want a step-by-step plan and professional disputes handled monthly:

start here by clicking on the following link to schedule your Free Consultation: https://api.leadconnectorhq.com/widget/groups/parker-method-group?user_id=hYwutz9Tej2kp6gpI6rH

Author

Charles Parker is a credit repair professional with over 16 years of experience helping consumers identify inaccurate and misleading credit reporting. Results vary and are not guaranteed.

Protecting the reporting clock matters because it determines how long a collection can legally remain on a credit report. When that date is mishandled, consumers can lose years of progress they didn’t need to lose.

A disciplined review process also prevents accidental admissions. What you say, when you say it, and how it’s documented can influence how the account is updated later.